Blockchain technology in banking relies on its strong verification capabilities to reduce the risk of bad loans and ensure borrowers are not fraudulent. This enhances banks’ know-your-customer (KYC) and anti-money-laundering (AML) capabilities.

Additionally, blockchain can serve as an immutable ledger that can make bank accounts more secure, accessible, and cheaper to maintain while minimizing the risks of bank runs. Through the use of interconnected blocks that contain verified transactions, blockchain technology allows secure and transparent transactions between parties without the need for intermediaries such as banks.

As such, banks are increasingly adopting blockchain technology in various use cases to streamline and enhance their services. We explore the benefits and use cases of blockchain technology in banking.

Benefits Of Blockchain In Banking

Blockchain technology can revolutionize traditional banking by providing a secure and trustless ledger system. This technology ensures robust verification capabilities, reduces the risk of bad loans, boosts banks’ know-your-customer (KYC) and anti-money-laundering (AML) capabilities, and can alleviate the risk of bank runs.

Blockchain’s ability to store immutable records can have a profound effect on how accounting, bookkeeping, and audit are done across the banking sector.

Improved Verification Capabilities

Blockchain technology provides a robust verification system for banks that could substantially reduce the risk of bad loans. With blockchain, banks can verify the identity of individuals, ensuring they are not criminals or bad actors. This verification capability could assist banks in making better-informed lending decisions and reduce the risk of defaults.

Boost To Know-your-customer And Anti-money Laundering Capabilities

Blockchain technology can help banks improve their ‘know-your-customer’ (KYC) and anti-money laundering (AML) capabilities. With blockchain, banks can create a permanent record of customer data, including transactions and personal identification details. Thus, banks can track money laundering and other fraudulent activities with greater ease and accuracy.

More Secure, Accessible And Cheaper Bank Accounts

Blockchain technology has the potential to make bank accounts more secure, accessible and cheaper to maintain. With blockchain, bank accounts could be represented on a decentralized ledger and make them more resistant to hacks and attacks. Banks could also eliminate intermediaries, which means fewer fees, faster transactions, and improved accessibility.

Reducing The Risk Of Bank Runs

Another advantage of blockchain technology is its potential to alleviate the risk of bank runs. With blockchain, banks could create a permanent record of deposits that clients make on their accounts, ensuring that depositors have a full and accurate view of their account balances. This transparency could reduce customer anxiety and fear of losing their deposits and hence reduce the risk of bank runs.

Transforming Accounting, Bookkeeping And Audit

Blockchain technology can transform accounting, bookkeeping and audit processes in banks. With blockchain, banks can accurately track financial transactions, providing a transparent and immutable audit trail. Additionally, blockchain can automate many financial processes, replacing manual tasks with smart-contracts and reducing the costs of financial services.

In conclusion, blockchain technology has the potential to revolutionize traditional banking and improve the way banks handle transactions, lending, and compliance. By leveraging blockchain’s benefits, banks can enhance their customer experience, securely store financial data, streamline transactions, reduce fees, and eliminate the need for intermediaries.

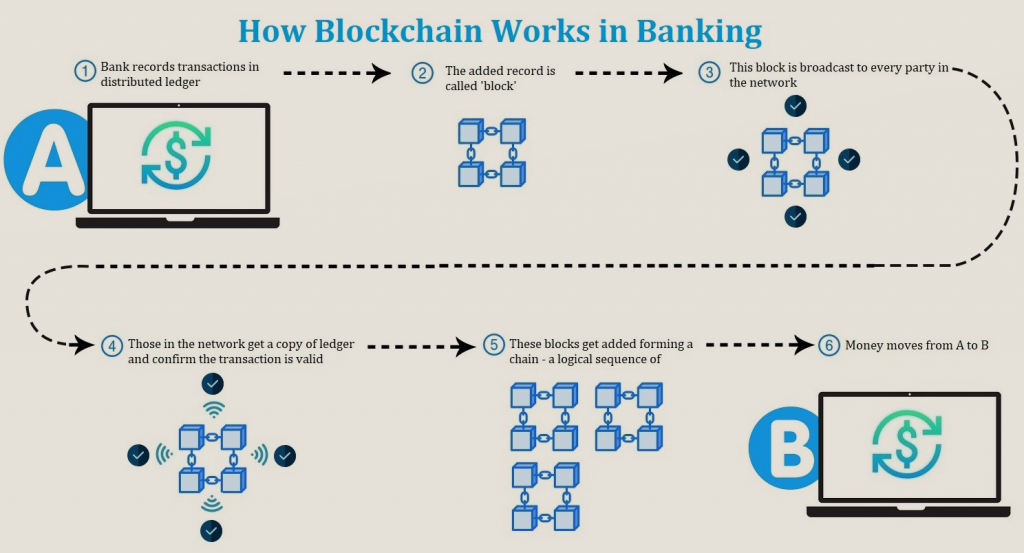

How Blockchain Works In Banking

Blockchain technology can revolutionize banking by providing robust verification capabilities that can reduce the risk of bad loans. It can also enhance banks’ know-your-customer (KYC) and anti-money-laundering (AML) capabilities by ensuring borrowers are not bad actors or criminals. With blockchain’s decentralized and secure ledger system, bank accounts can be represented on blockchains, making them more secure, accessible, and cheaper to maintain, alleviating the risk of bank runs.

Decentralised And Distributed Ledger System

Blockchain technology in banking eliminates the need for central authorities such as banks, governments, or financial institutions to verify transactions. Decentralized and distributed ledger systems allow transactions to occur between two parties directly, offering a secure and transparent method of conducting transactions. In a blockchain network, every node holds a copy of the ledger, making it accessible to everyone and nearly impossible to hack. This eliminates the need for intermediaries, resulting in faster transactions, lower fees, and increased efficiency.

Interconnected Blocks Containing Transaction Records

A blockchain is a series of interconnected blocks containing transaction records. Each block in the blockchain holds a set of transaction records, and each subsequent block is connected to the previous block using cryptographic techniques. This creates an immutability factor that verifies that the previous block data is unchanged. Once a block is added to the chain, it cannot be changed or tampered with, ensuring a high level of security for each transaction.

Immutable And Chronological Chain Of Information

Blockchain technology creates an immutable and chronological chain of information that is transparent, secure, and verifiable. Each transaction record is timestamped in sequential order, creating a transparent and chronological chain of data that is nearly impossible to manipulate. This makes blockchain technology an ideal solution for any industry that requires transparency, accountability, and accuracy.

Cryptographic Techniques Used For Linking Blocks

In a blockchain network, cryptographic techniques, such as SHA256 hashing, are used to link each block to the previous block. This creates a digital fingerprint of each block that ensures the integrity and immutability of the data. Cryptography also takes care of all data transmission and provides encryption, ensuring that any third-party interference is neutralized, and the data remains secure.

Using blockchain technology in banking ensures the security and transparency of every transaction. The decentralized and distributed ledger system, interconnected blocks, immutability and chronological chain of information, and cryptographic techniques used for linking blocks are the essential features of blockchain that provide the necessary security and transparency for financial transactions.

Use Cases Of Blockchain In Financial World

The use of blockchain technology in the financial world has revolutionized banking systems and how transactions are carried out. Blockchain technology has brought about a decentralized and secure system that has given banks leverage in their activities. Here are some of the use cases of blockchain technology in the financial world:

Public And Private Blockchains Implementation

The implementation of public and private blockchains has been a significant use case of blockchain technology in the financial world. Public blockchains are accessible to everyone, while private blockchains are accessible to only designated personnel. This feature has made blockchain implementation in the banking system more secure and more transparent.

Storing Information About Transactions

Blockchain technology has made it possible to store information about transactions in a secure and immutable manner. This feature has reduced the risk of fraud or manipulation of transactions. The transparency of the system has also made it easier for regulators to detect and prevent financial crimes.

Revolutionising The Banking System By Building A Decentralised Database Of Digital Assets

The banking system has always faced challenges in managing digital assets effectively. With blockchain technology, a decentralized database of digital assets can be built. This system will make it possible for banks to manage digital assets securely and efficiently, ultimately reducing the cost of managing assets.

Opening Up New Sectors Of Banking

Blockchain technology has opened up new sectors of banking, such as peer-to-peer lending, crowd-funding, and micropayments. This innovation has provided more opportunities for small businesses and individuals to access financial services and investments.

Overall, blockchain technology has brought significant benefits to the banking system, and it will continue to shape the future of banking. By adopting blockchain technology, banks can enjoy greater security, efficiency, and transparency in their transactions.

Potential Impact Of Blockchain On Traditional Banking

Blockchain technology has the potential to revolutionize traditional banking by providing a more secure and transparent way of verifying transactions. With its robust verification capabilities, blockchain can reduce the risk of bad loans and enhance banks’ know-your-customer and anti-money-laundering capabilities, while also making bank accounts more secure and accessible.

Blockchain technology is rapidly gaining popularity among financial institutions and is considered one of the most significant technological advancements in the financial industry. Blockchain has the potential to transform the traditional banking industry in many ways. In this article, we will be focusing on the potential impact of blockchain on traditional banking under the following headings:

Reduced Risk Of Bad Loans

Bad loans can cause significant damage to banks, leading to credit losses and reputation damage. However, with blockchain, banks could reduce the risk of bad loans by utilizing the technology’s robust verification capabilities. Blockchain can make sure that borrowers are not criminals or bad actors, ultimately reducing the risk of default for banks. Furthermore, blockchain can assist banks in streamlining their credit underwriting processes by automating verification of borrower data, such as financial statements, credit history, income, and assets, leading to improved risk management for banks.

Boosting The Financial Inclusion

Due to regulatory requirements, legacy banking systems can be exclusionary, limiting access to financial services for underbanked and unbanked populations. Blockchain technology can facilitate financial inclusion by providing financial services to populations that are underserved by traditional banking systems. Blockchain-based banking services can assist in reducing overhead costs for banks, which, in turn, could lead to reduced fees that the underbanked and unbanked populations can afford.

Revolutionising The Fundamental Business Model Of Banking

Blockchain technology provides opportunities for fundamental changes to the banking industry’s business model. Through tokenization, securities, and other financial assets can be issued, traded, and settled with greater transparency and efficiency. Furthermore, smart contracts could replace traditional intermediaries in transactions such as loan origination, funds transfer, and trade finance, leading to faster and cheaper transactions, reduced friction in financial markets, and increased liquidity.

Alleviating Financial Market Volatility

The financial markets are susceptible to high levels of volatility, leading to significant losses for market participants. Blockchain technology’s transparency and immutability can mitigate the risk of market manipulation and provide greater certainty in financial markets. Asset tokenization on blockchain platforms can also allow for fractional ownership of assets, thereby reducing concentration risk and increasing market stability.

In conclusion, blockchain technology has the potential to revolutionize the traditional banking industry. With its enhanced security, immutability, and transparency, blockchain could transform the way banking is conducted, leading to greater efficiency, financial inclusion, and reduced risk. As the technology continues to mature, it is expected that more financial institutions will adopt blockchain technology, leading to further innovation and transformation of the financial industry.

Challenges And Opportunities Of Blockchain In Banking

Blockchain technology presents both challenges and opportunities for banking. One major benefit is the ability to increase security and efficiency in financial transactions. This helps improve customer experience, while reducing risk of fraud and bad loans. Furthermore, blockchain can bolster anti-money laundering and know-your-customer capabilities.

Challenges and Opportunities of Blockchain in Banking

Blockchain technology is gaining popularity in various sectors due to its ability to provide secure and transparent transactions between two parties without the need for a trusted intermediary. In the banking industry, blockchain technology has the potential to transform traditional banking by improving operational efficiency and reducing costs. However, there are still some challenges that the banking industry needs to address in the adoption of blockchain technology.

Legal And Regulatory Landscape

There is still a legal and regulatory gap that needs to be addressed in the banking industry for the adoption of blockchain technology. This gap is due to the lack of standardization and regulations governing blockchain technology. The regulatory authorities need to develop a comprehensive framework for regulating blockchain-based transactions, including the exchange of digital tokens and cryptocurrencies. Currently, there is no universal definition of blockchain for regulatory purposes. Therefore, the regulatory authorities need to provide clear guidance on how blockchain technology can be integrated into existing legal and regulatory frameworks.

Integration With Existing Systems And Technologies

The adoption of blockchain technology presents a challenge in terms of integrating it into existing banking systems and technologies. Most banks have already invested a significant amount of resources in developing their systems and technologies, which may not be compatible with blockchain technology. Banks need to find a way to integrate blockchain technology with their existing systems and technologies seamlessly. Moreover, the integration of blockchain technology into existing systems should not lead to a reduction in usability and functionality.

Scalability And Interoperability Issues

A critical challenge facing blockchain technology is scalability and interoperability. Blockchain technology relies on a distributed network of computers to verify transactions, which can cause scalability issues. The more nodes on the network, the slower the transaction processing time becomes. Banks need to find ways to ensure that blockchain technology can handle a large volume of transactions without compromising speed. Furthermore, blockchain technology needs to be interoperable with other existing systems, such as SWIFT and SEPA, to ensure seamless connectivity between different banking systems.

In conclusion, blockchain technology has the potential to revolutionize the banking industry by reducing costs and improving operational efficiency. However, banks need to address several challenges, such as legal and regulatory gaps, integration with existing systems, and scalability issues. Overcoming these challenges will enable banks to leverage the benefits of blockchain technology and stay ahead of the competition.

:max_bytes(150000):strip_icc()/Blockchain_final-086b5b7b9ef74ecf9f20fe627dba1e34.png)

Frequently Asked Questions On How Blockchain Works In Banking

How Is Blockchain Used In Banks?

Blockchain technology is used in banks for its robust verification capabilities, which can reduce the risk of bad loans. It also enables banks to boost their know-your-customer (KYC) and anti-money-laundering (AML) capabilities by ensuring that borrowers are not criminals or bad actors.

In addition, blockchain can make bank accounts more secure, accessible, and less expensive to maintain by representing them on the blockchain ledger.

How Blockchain Can Solve The Banking Problem?

Blockchain can solve the banking problem by providing a secure and decentralized ledger, reducing the risk of bad loans and aiding banks’ know-your-customer and anti-money-laundering capabilities. It can potentially represent bank accounts on blockchains, making them more secure, accessible and cheaper to maintain, while also alleviating the risk of bank runs.

Blockchain’s ability to store immutable records can have a profound effect on accounting, bookkeeping and audit in the banking sector.

How Blockchain Works Step By Step?

Blockchain technology is a decentralized, distributed ledger system that uses cryptographic techniques to store a series of interconnected blocks containing transaction records. In banking, blockchain’s robust verification capabilities can reduce the risk of bad loans, improve banks’ KYC and AML capabilities, and potentially allow for more secure, accessible, and cheaper bank accounts.

The structure of a blockchain in banking consists of a chain of blocks, each containing a set of data that is linked together chronologically.

What Is The Structure Of A Blockchain In Banking?

The structure of a blockchain in banking is a distributed, immutable, and decentralized ledger that contains a chain of blocks, with each block having a set of data. Blocks are linked together using cryptographic techniques to form a chronological chain of information.

It enhances banks’ know-your-customer (KYC) and anti-money laundering (AML) capabilities and reduces the risk of bad loans while also making bank accounts more secure and accessible.

Conclusion

Blockchain technology has revolutionized the banking sector by enabling secure and transparent transactions without intermediaries. With its robust verification capabilities, blockchain technology has the potential to reduce the risks of bad loans and improve banks’ KYC and AML capabilities. The ability to store immutable records could also transform accounting, bookkeeping, and audit practices across the sector.

Blockchain technology in banking is a game-changer that could improve efficiency, security, and transparency, ultimately benefiting customers and the industry as a whole.