Blockchains are created through the use of energy-intensive mining nodes to validate transactions, add them to the block they are building and then broadcast the completed block to other nodes. Various time-stamping schemes, such as proof-of-work, are used to serialize changes.

Consensus methods, such as proof of stake, are later implemented for more efficiency. Blockchain technology has taken the world by storm, and its relevance in various industries continues to grow. It has transformed the way data is stored and shared, providing a decentralized, transparent and secure platform for transactions.

Many people wonder how blockchains are created and what makes them secure. We will delve into the process of creating a blockchain, the technology behind it, and the relevance of blockchain in modern times. Whether you are an enthusiast or a novice in the field, this guide will provide you with a comprehensive understanding of blockchain technology.

What Are Blockchains Built On?

Blockchains are built using cryptography, decentralization, and a consensus mechanism. These three principles work together to create a highly secure system that is nearly impossible to tamper with. By utilizing these technologies, blockchains can be created and maintained, allowing for secure transactions and data storage.

What Are Blockchains Built On?

Blockchains, the backbone of cryptocurrencies, are based on a foundation of principles of cryptography, decentralization, and consensus. These three principles ensure that data is protected, secure, and feasible for transactions to occur without any authoritative entities. Additionally, blockchains have a highly secure underlying software system that makes them immune to cyber-attacks. Furthermore, blockchains do not have a single point of failure, ensuring that there is no breach in the security of the data stored in the blockchain. Let’s take a closer look at each of these principles.

Principles of Cryptography

Cryptography is the method of securing communication from third-party interference or unauthorized access. In the context of blockchains, cryptography involves using complex algorithms and protocols to encrypt data and ensure the integrity, confidentiality, and authenticity of the information stored within the blockchain. Cryptographic hashes are utilized in the blockchain to create digital signatures that guarantee the authenticity of transactions.

Decentralization

Decentralization is the process of ensuring that the control of the system’s operation is distributed in various locations rather than being centralized in one place. Decentralization ensures that there is no central authority in control of the blockchain, resulting in better security, trust, and transparency. Anyone can access and participate in a decentralized blockchain system without any restrictions.

Consensus

Consensus refers to the process of agreeing on a set of rules that everyone involved adheres to. In the context of blockchains, consensus ensures that every participant in the network shares the same database, creating a single common source of truth. Consensus protocols ensure that transaction verification by different nodes is achieved through a democratic process that validates the transaction before being added to the blockchain.

Highly Secure Underlying Software System

Blockchains are built on a highly secure underlying software system that forms the foundation of blockchain technology. These software systems are designed to ensure immutability, fault-tolerance, efficiency, and scalability.

No Single Point of Failure

Blockchains do not have a central entity in control, so they do not have a single point of failure. Each node holds a copy of the blockchain database and validates the transaction before adding it to the blockchain. In the event of any attacks or failures, the blockchain remains intact, and the users can continue to transact seamlessly.

In conclusion, blockchains’ inherent properties such as principles of cryptography, decentralization, and consensus ensure a secure, transparent, and decentralized system. Additionally, the highly secure underlying software system and the lack of a single point of failure make blockchains one of the most promising technologies for decentralized applications and peer-to-peer transactions.

How Are Blockchains Formed?

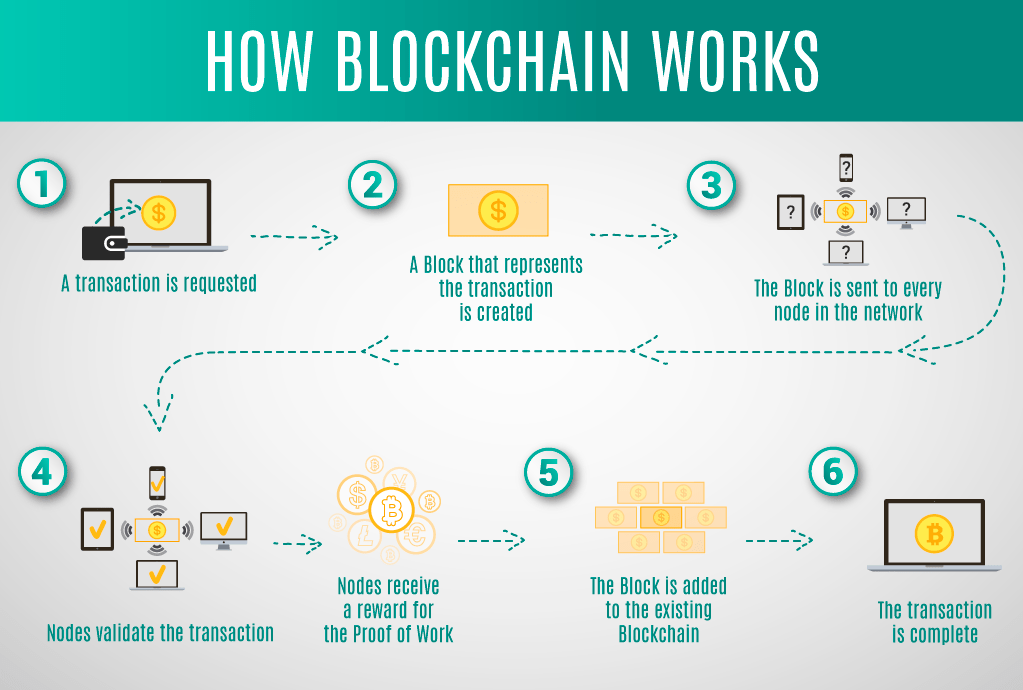

Blockchains are created through a process called mining, where individual nodes in a network validate transactions and add them to the current block being built. Once completed, this block is broadcasted to other nodes in the network. The timestamping scheme used in blockchains is proof-of-work, which helps to serialize changes and maintain security.

ockchains are formed through a proof-of-work time-stamping scheme that helps ensure the accuracy and security of each transaction. As a transaction is made, it is packaged into a block and then validated by a network of miners who must use a significant amount of energy to solve a complex mathematical problem before the block can be added to the chain. This energy-intensive process is necessary to prevent fraudulent activity and ensure that each block is securely linked to the previous one.

Energy-Intensive Mining Nodes to Validate Transactions

Early blockchains rely heavily on energy-intensive mining nodes to validate transactions and create new blocks. These nodes are responsible for solving complex mathematical problems that can only be solved through trial-and-error, which requires a significant amount of computational power and energy. Once a miner solves the problem and confirms the transaction, the block is added to the chain and broadcast to other nodes. While this process is secure, it is also slow and expensive, making it difficult for early blockchains to scale.

Proof-of-Work Time-Stamping Scheme

With a proof-of-work time-stamping scheme, every transaction is time-stamped and linked to the previous transaction on the chain. This creates an unalterable record of each transaction that is nearly impossible to tamper with. To ensure that each new block is added to the chain only after a significant amount of computational work has been done, miners must solve complex mathematical problems that require a significant amount of energy. This ensures the security and integrity of the blockchain, but it also makes the process of validating transactions slow and expensive.

Later Consensus Methods Include Proof of Stake

To address the scalability issues associated with energy-intensive mining nodes, newer blockchain designs have switched to other consensus methods such as proof of stake. With this approach, miners are required to stake their own cryptocurrency as collateral to participate in the validation process. This eliminates the need for energy-intensive mining nodes, enabling transactions to be confirmed much more quickly and cost-effectively. Additionally, this approach is more eco-friendly and less resource-intensive.

In conclusion, blockchains are formed using a proof-of-work time-stamping scheme that helps ensure the accuracy and security of each transaction. While early blockchains rely heavily on energy-intensive mining nodes, newer designs have switched to alternative consensus methods like proof of stake that are more energy-efficient and scalable. Through these various methods, blockchain technology provides an unalterable and secure record of every transaction, making it an ideal solution for numerous industries and applications.

How Are Blockchain Blocks Created?

Blockchains are created by mining nodes that validate transactions and add them to blocks. The blocks are then broadcasted to other nodes using proof-of-work or proof-of-stake consensus methods. These decentralized systems use cryptography to create secure and tamper-proof software that ensures the integrity of transactions.

Blockchain technology enables the creation of decentralized digital ledgers that store data without any central authority or intermediary. Blocks are fundamental building blocks of a blockchain that record transactions and data. Each block is linked with the previous block, forming a chain of blocks, i.e., a blockchain. Blocks play a critical role in ensuring the integrity and security of the network. The process of creating a block is called mining, which involves solving a complex mathematical puzzle using computational power.

Blocks Are Fundamental Building Blocks Of A Blockchain

Blocks are the building blocks of a blockchain that store data and details about transactions. Each block is identified by a unique hash and timestamp and is linked with the previous block, forming a chain. This linking system and the use of cryptographic hash functions ensure that data stored on a blockchain is tamper-proof and secure.

Critical Role In Ensuring Integrity And Security Of Network

Blocks play a critical role in ensuring the integrity and security of a blockchain network. The use of cryptography and the linking of blocks guarantee that once a block is added to the blockchain, it cannot be altered or deleted without altering the entire chain. It means that every block is linked to the previous and following blocks in an unbreakable chain.

Process Of Creating A Block Is Called Mining

Mining is the process by which a new block is created on a blockchain. It involves solving a complex mathematical puzzle that requires substantial computational power. The goal of this puzzle is to provide a secure and trustless way to add transactions to the blockchain. The first miner to solve the puzzle adds a new block to the blockchain and receives a reward in the form of cryptocurrency.

To conclude, blocks play a crucial role in creating and maintaining blockchain networks. Their secure, immutable data storage design provides a tamper-proof, trustless environment where transactions can be added and verified without the need for intermediaries. The mining process of creating blocks ensures security and helps to maintain the blockchain’s integrity by incentivizing miners to follow the rules.

Which Programming Language Is Used In Blockchain?

Blockchain technology is created through the use of programming languages such as Solidity, Java, Python, and C++. These languages are used to write “smart contracts” that are uploaded onto the blockchain and executed automatically. The choice of programming language depends on the specific blockchain platform being used, such as Ethereum or Hyperledger.

Which Programming Language Is Used in Blockchain?

In order to create blockchains, the use of programming languages is essential. This is because blockchains are essentially a collection of computer code that runs on a network of computers. There are several programming languages that are commonly used in blockchain development. Some of the most popular ones include Java, JavaScript, C++, Python, PHP, Go, Ruby and Solidity.

Java: Java is a popular programming language that has been used extensively in blockchain development. One of the main advantages of using Java is that it is easy to use and understand. Additionally, Java has a large community of developers who can provide support and help in the development process.

JavaScript: JavaScript is another popular programming language that is used in blockchain development. Its popularity can be attributed to the fact that it is a versatile language that can be used in both frontend and backend development. Additionally, JavaScript is easy to learn and has a large community of developers.

C++: C++ is a programming language that is used in many different areas of computer science, including blockchain development. The advantage of using C++ in blockchain development is that it is a low-level language that provides developers with a high degree of control over the code they write.

Python: Python is a popular programming language that is used in many different areas of computer science. Its popularity in blockchain development can be attributed to the fact that it is a beginner-friendly language that is easy to learn. Additionally, Python has a large community of developers who can provide support and help in the development process.

PHP: PHP is a server-side scripting language that is used in many different areas of web development. Its popularity in blockchain development can be attributed to the fact that it is a beginner-friendly language that is easy to learn. Additionally, PHP has a large community of developers who can provide support and help in the development process.

Go: Go is a relatively new programming language that is becoming increasingly popular in blockchain development. Its popularity can be attributed to the fact that it is a fast and efficient language that is easy to learn. Additionally, Go has a large community of developers who can provide support and help in the development process.

Ruby: Ruby is a programming language that is used in many different areas of computer science. Its popularity in blockchain development can be attributed to the fact that it is a beginner-friendly language that is easy to learn. Additionally, Ruby has a large community of developers who can provide support and help in the development process.

Solidity: Solidity is a programming language that is specifically designed for blockchain development. It is used to write smart contracts, which are self-executing contracts that can be used to encode the rules and penalties of an agreement. The advantage of using Solidity in blockchain development is that it is a purpose-built language that is well-suited to the task at hand.

Each language has its own unique features and benefits. The choice of language depends on specific project requirements. For example, if a project requires high performance and low-level control, C++ may be the best choice. On the other hand, if a project requires a high degree of flexibility, JavaScript may be the best choice. Ultimately, the choice of language will depend on the specific needs of the project at hand.

How To Create A Blockchain For Record Keeping?

To create a blockchain for record keeping, you have two options. You can use an existing blockchain like Ethereum, where you define your Smart Contract and interface to access it. Or alternatively, you can create your private blockchain using Hyperledger Fabric, which provides added control over access and lets you deploy Smart Contracts that meet your record-keeping needs.

ckchain, and create new blocks. However, there are different ways to create a blockchain for record keeping, depending on your specific needs. In this post, we will explore some of the options you have to create a blockchain for record keeping, including using an existing blockchain like Ethereum, creating a private blockchain with Hyperledger Fabric, and deploying your own smart contracts. Let’s dive in!

Using An Existing Blockchain Like Ethereum

If you are looking for a quick and easy way to create a blockchain for record keeping, using an existing blockchain like Ethereum may be the way to go. Ethereum is a popular blockchain platform that allows you to create your own smart contracts and decentralized applications (dApps) on top of its blockchain infrastructure.

To use Ethereum for record keeping, you will need to pay some Ethers, which are the platform’s native cryptocurrency. Once you have some Ethers, you can deploy your smart contract on the Ethereum network and start using it for record keeping. However, keep in mind that your smart contract will be publicly visible and accessible to anyone on the Ethereum network.

Creating A Private Blockchain With Hyperledger Fabric

If you need more control over your record-keeping blockchain and want to keep it private, you can create your own blockchain with Hyperledger Fabric. Hyperledger Fabric is a blockchain infrastructure that allows you to create custom private blockchains and smart contracts for your specific needs.

With Hyperledger Fabric, you can define who has access to your blockchain and what kind of data can be stored on it. You can also define the rules and permissions for your smart contracts. This makes Hyperledger Fabric a great option for record-keeping applications that require privacy and security.

Deploying Your Own Smart Contracts

Whether you decide to use an existing blockchain like Ethereum or create your own private blockchain with Hyperledger Fabric, you will need to deploy your own smart contract to implement your record-keeping system.

A smart contract is a program that runs on the blockchain and defines the rules and logic for your record-keeping system. You can define what kind of data can be stored on your blockchain, who can access it, and what kind of actions can be performed on it.

Once you have deployed your smart contract, you can start using it for record keeping. However, you will also need to define an interface to call your blockchain. This ensures that other applications can interact with your blockchain and that your record-keeping system is easy to use and integrate with other systems.

In conclusion, creating a blockchain for record keeping can be done in different ways, depending on your specific needs. Whether you decide to use an existing blockchain like Ethereum or create your own private blockchain with Hyperledger Fabric, the process involves deploying your own smart contract and defining an interface to call your blockchain. By choosing the right blockchain platform and smart contract, you can build a reliable and secure record-keeping system that meets your specific requirements.

How Blockchain Can Help In Energy?

Microgeneration of electricity is becoming a huge trend in the power generation business. New energy initiatives such as home power generation and community solar power are filling in gaps of power supply across the world. As microgeneration adds to traditional power suppliers, it fosters creation of an energy market.

Blockchain Can Enable Consumption Of Surplus Energy In A Different Location

Smart meters can register produced and consumed electricity in a blockchain, which allows for consumption of the surplus energy in a different location, providing credits or currency to the original producer. The credits can then be redeemed against the grid when the microgenerator needs additional electricity from the grid.

Microgeneration Of Electricity Is Becoming A Huge Trend In The Power Generation Business

With blockchain technology, microgeneration of electricity can be sold directly to customers, cutting out the middleman and decreasing reliance on centralised power suppliers. This creates an energy market with minimal red tape, ensuring fair transactions and equitable distribution of resources.

Smart Meters Can Register Produced And Consumed Electricity In A Blockchain

The use of smart meters integrated with blockchain enables the automatic recording of energy transactions, leading to more transparent and accurate billing. Consumers can monitor and control their energy consumption in real-time, making it easier to manage usage and reduce overall energy costs. Additionally, utility companies can use the recorded data to optimise energy distribution and reduce waste.

Popular Blockchain Platforms

Blockchain platforms like Ethereum, Hyperledger Fabric, and TRON offer various ways to create and deploy customized blockchains for a wide range of applications. These platforms rely on consensus algorithms to ensure the integrity of the data stored on the blockchain, and they also provide tools and frameworks for building decentralized applications that leverage the power of blockchain technology.

ork, to create a secure and decentralized ledger. Popular blockchain platforms such as Ethereum, Hyperledger Fabric, Consensys, TRON, Stellar, Ripple, Hashgraph, and NEO have made it possible for everyone to create their own blockchain network or utilize an existing one. Let’s take a closer look at these popular blockchain platforms and their features.

Ethereum

Ethereum, launched in 2015, is one of the most popular blockchain platforms that allows developers to create and deploy their decentralized applications (dApps). Ethereum’s smart contract functionality and its programming language Solidity make it ideal for building complex blockchain solutions. The platform uses its cryptocurrency called Ether (ETH) as a reward for mining new blocks, processing transactions, and running smart contracts.

Hyperledger Fabric

Hyperledger Fabric was initially launched in 2016 by the Linux Foundation and is an open-source blockchain project that aims to improve enterprise blockchain solutions. The platform offers modular architecture, high scalability, and privacy, making it an ideal choice for industries such as finance, healthcare, and supply chain management. Hyperledger Fabric also provides support for smart contracts and Chaincode, its native programming language.

Consensys

Consensys is a blockchain software company that provides robust solutions to entrepreneurs and enterprises alike. The platform offers a suite of products that help users develop, deploy, and manage smart contracts and dApps on the Ethereum network. Consensys also provides tools for auditing and optimizing smart contracts, ensuring the security of the blockchain network.

Tron

TRON is a blockchain-based platform that focuses on content distribution and sharing. It uses Tronix (TRX) as its cryptocurrency, which helps reward content creators and ensures secure payments. TRON’s blockchain network can handle up to 2,000 transactions per second (TPS), making it faster than Ethereum.

Stellar

Stellar is an open-source platform that aims to facilitate cross-border transactions and make it more accessible to everyone. It uses its cryptocurrency Lumens (XLM) to facilitate transactions and operations on its network. Stellar’s blockchain protocol also uses a consensus algorithm that allows for faster and more efficient validation of transactions.

Ripple

Ripple is a blockchain platform that helps financial institutions and banks transfer money across borders. It offers real-time gross settlement and currency exchange with low transaction fees. Ripple uses its digital currency called XRP to enable fast and secure transactions.

Hashgraph

Hashgraph is a distributed ledger technology that aims to provide a more efficient and decentralized alternative to traditional blockchain networks. It uses a consensus algorithm that allows for lightning-fast transaction processing and high throughput.

Neo

NEO is a Chinese blockchain platform that allows The development of digital assets and smart contracts. It offers lower fees and higher scalability than Ethereum and uses Delegated Byzantine Fault Tolerance (dBFT) as its consensus algorithm. NEO’s cryptocurrency is called GAS, which helps pay for transaction and executing smart contracts on its network.

In conclusion, these popular blockchain platforms have made it possible for everyone to easily create their blockchain network or join an existing one. Each blockchain platform offers unique features that cater to specific industries and use cases, making it crucial to choose the right platform to achieve business objectives.

Frequently Asked Questions Of How Are Blockchains Created

How Are Blockchains Formed?

Blockchain is formed through the validation and serialization of transactions by energy-intensive mining nodes, which are then broadcasted to other nodes. This process uses time-stamping schemes, such as proof-of-work, to ensure the security and decentralization of the system. Later methods may use proof of stake for consensus.

What Are Blockchains Built On?

Blockchains are built on the three principles of cryptography, decentralization, and consensus. These create a secure software system that is very difficult to tamper with. There is no single point of failure, and a single user cannot change the transaction records.

How Are Blockchain Blocks Created?

Blockchain block involves validation of transactions through a consensus mechanism, followed by adding the validated transactions to a new block and solving a cryptographic puzzle to create a unique block hash. Once created, the block is added to the existing chain of blocks in a sequential manner, forming the immutable blockchain ledger.

Which Programming Language Is Used In Blockchain?

The programming language used in blockchain varies depending on the platform. Ethereum, for example, uses Solidity, while Hyperledger Fabric uses Go or Java. Consensus methods such as proof of work or proof of stake also play a role in how blocks are created.

Conclusion

Creating a blockchain is an intricate process that requires careful attention to detail. Through the use of complex algorithms and consensus methods, multiple nodes are able to come to an agreement on the validity of transactions. These transactions are then added to a block, which is verified and added to the blockchain.

The decentralization and security provided by blockchain technology have numerous applications across various industries. As the world continues to advance, so too will the development and growth of blockchain technology.