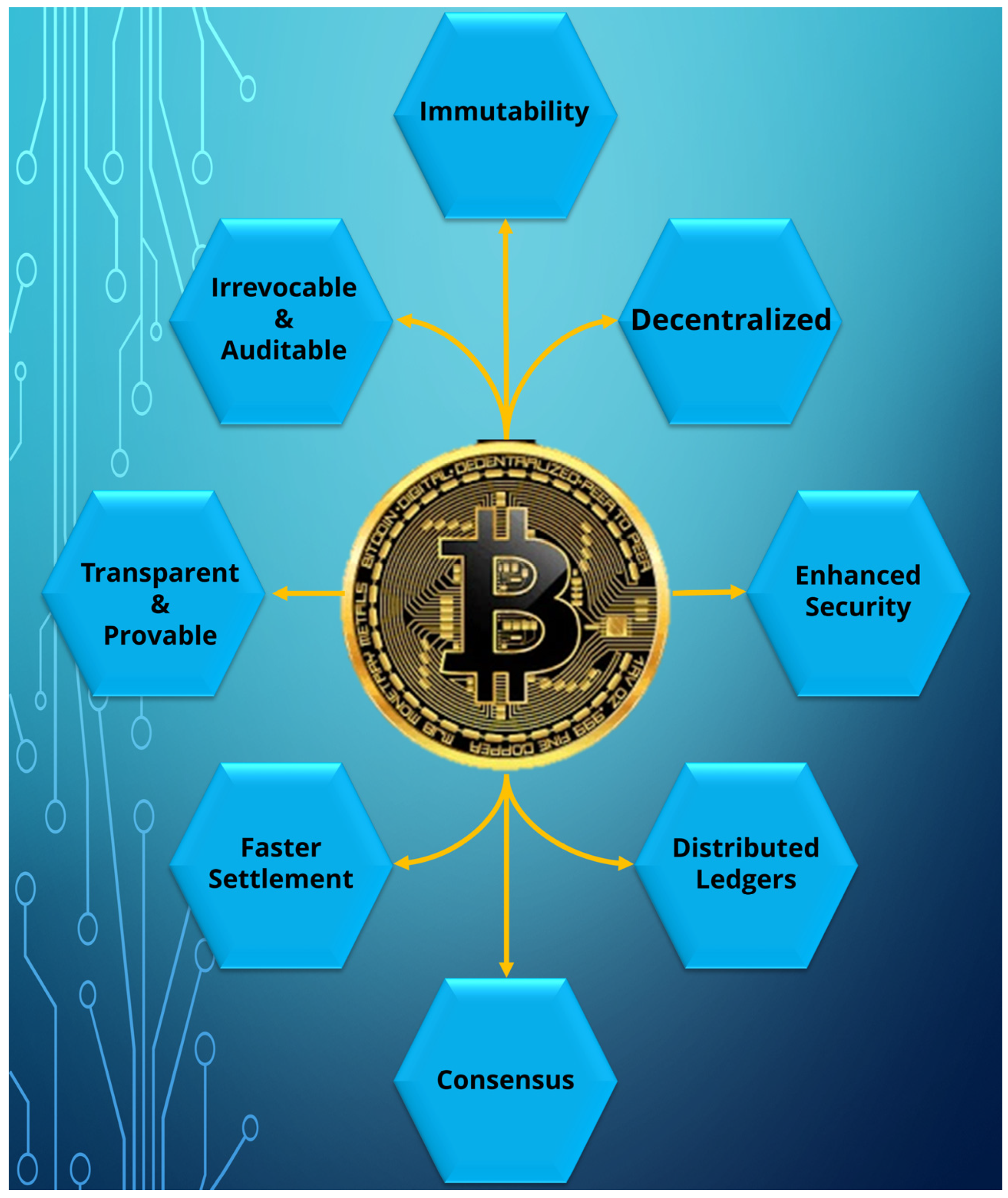

Blockchain uses consensus mechanisms like Proof of Work to prevent double spending by validating transactions. Blockchain technology is built on the concept of decentralization and transparency.

It ensures that each transaction is confirmed by multiple parties, eliminating the risk of double spending without the need for a central authority. By recording transactions in chronological order and linking them in a chain, blockchain creates a secure and immutable ledger.

This innovation has revolutionized various industries by offering secure, transparent, and efficient ways to transfer value without the risk of fraud or duplication. With its decentralized nature and cryptographic security, blockchain has become a powerful tool in preventing double spending and ensuring trust in digital transactions.

The Basics Of Blockchain Technology

Blockchain technology prevents double spending through its decentralized and distributed ledger system. Each transaction is immutable and recorded on blocks, ensuring transparency and security. Blockchain eliminates the need for intermediaries and cuts costs significantly. It uses cryptography to secure transactions across the network.

Understanding Double Spending

To prevent double spending in blockchain, it’s crucial to understand the concept thoroughly. Double spending occurs when the same digital currency is used more than once due to a lack of central authority overseeing transactions. Blockchain technology combats this by ensuring each transaction is verified and recorded in a decentralized and transparent manner.

| Double Spending: | When a digital currency is spent more than once because of its digital nature. |

| Challenges: | Traditional payment systems lack security mechanisms to prevent double spending. |

Blockchain technology solves the issue by decentralizing transactions. It ensures each transaction is unique and cannot be duplicated. This prevents fraudulent activities in digital transactions. Blockchain maintains a secure ledger of transactions, making it impossible to spend the same funds twice.

Blockchain’s Solution To Double Spending

Blockchain technology prevents double spending by utilizing consensus mechanisms to validate and secure transactions. This decentralized and transparent system ensures that each transaction is immutable, creating a tamper-proof and trustless environment. By maintaining an immutable transaction history, blockchain effectively eliminates the risk of double spending, providing a secure and reliable platform for financial transactions. The decentralized nature of blockchain and its consensus mechanisms make it nearly impossible to counterfeit or manipulate transaction records, establishing a level of trust and security that traditional centralized systems cannot match.

Maximizing Security In Blockchain

Blockchain technology is revolutionizing the way transactions are conducted online. One of its key features is preventing double spending, which is a major concern in digital transactions. Through the use of cryptography and digital signatures, blockchain ensures the security and integrity of each transaction. Cryptography protects the privacy and confidentiality of data by encrypting it. Digital signatures verify the authenticity and integrity of transactions, ensuring that they cannot be tampered with.

Smart contracts, another aspect of blockchain technology, are self-executing contracts with the terms of the agreement directly written into code. This eliminates the need for intermediaries and maximizes security. With blockchain, transactions are secure, transparent, immutable, and resistant to fraud. With the increasing popularity of cryptocurrencies and online transactions, blockchain is becoming more important than ever in preventing double spending and ensuring the integrity of digital transactions.

Building Trust With Blockchain

Blockchain technology prevents double spending by building trust through transparency and traceability. With traditional financial systems, there is a risk of someone making multiple transactions with the same funds, resulting in fraud. However, with blockchain, each transaction is recorded on a public ledger, visible to all participants. This transparency ensures that everyone can see the history of every transaction, making it virtually impossible to duplicate or manipulate funds.

Additionally, blockchain reduces the need for intermediaries, such as banks or payment processors, which can introduce vulnerabilities for potential fraud. By removing these intermediaries, blockchain technology allows for direct and secure peer-to-peer transactions.

Moreover, the decentralized nature of blockchain ensures that no single entity has control over the system, making it highly resistant to hacking and fraud. Each transaction is verified by multiple participants in the network, adding an additional layer of security and reducing the risk of double spending.

In conclusion, blockchain technology revolutionizes trust by providing a transparent and secure system for preventing double spending and reducing fraud. Its transparency and traceability, coupled with the elimination of intermediaries, make blockchain an innovative solution for building trust in various industries.

Real-world Applications Of Blockchain To Prevent Double Spending

Blockchain technology has real-world applications in preventing double spending. Cryptocurrencies utilize blockchain to secure transactions and prevent fraudulent double spending. The immutable nature of blockchain ensures that transactions cannot be altered, enhancing security. Additionally, in supply chain management, blockchain’s transparent and traceable ledger can prevent double spending and counterfeiting. By recording transactions at each stage, supply chain participants can validate the authenticity of products and prevent the occurrence of double spending. This demonstrates the effectiveness of blockchain in providing security and integrity in various real-world applications.

Challenges And Future Developments

Blockchain technology has revolutionized financial transactions by preventing double spending, ensuring secure and transparent transactions. The challenges lie in scalability and integration with existing systems, but future developments aim to enhance efficiency and security. With ongoing innovation, blockchain technology is poised to transform various industries beyond finance.

| Blockchain technology faces challenges in scalability to prevent double spending. | |

| Scalability: Blockchain scalability is vital for handling large transaction volumes efficiently. | Regulatory Considerations: Regulations play a crucial role in shaping blockchain development. |

Frequently Asked Questions For Blockchain Prevent Double Spending

How Does Blockchain Prevent Double Spending?

Blockchain prevents double spending by using a decentralized network of computers called nodes to validate transactions. When a transaction occurs, it is added to a block and then permanently recorded on the blockchain. Once a transaction is recorded, it cannot be changed or tampered with, ensuring that the same funds are not spent more than once.

This makes blockchain a secure and reliable system for financial transactions.

Conclusion

Blockchain technology has proven itself as an effective solution to prevent double spending in digital transactions. Its decentralized nature, cryptographic algorithms, and consensus mechanism work together to ensure the security and integrity of transactions. As the adoption of blockchain continues to grow, it has the potential to revolutionize various industries and transform the way we conduct business in the digital age.