Crypto trading is taxed as a taxable event, where buying, selling, or exchanging cryptocurrency counts as a capital gain or loss. There is no tax for simply holding crypto, but you will need to report and pay taxes on crypto you’ve earned or sold.

Taxation Basics

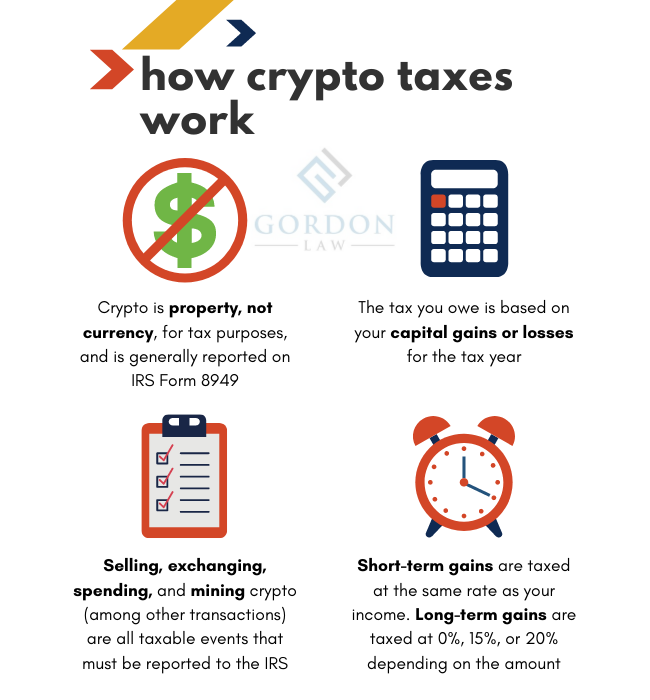

The IRS treats cryptocurrency as property, meaning that when you buy, sell or exchange it, this counts as a taxable event and typically results in either a capital gain or loss. There is no tax for simply holding crypto for US taxpayers. You will only report and pay taxes on crypto you’ve earned or which you purchased and later sold or exchanged for other crypto. You’re required to pay tax on the profit you made from your sale (total sale price of your cryptocurrency minus original purchase price), commensurate with your personal tax bracket.

Tax Implications

Capital Gains and Losses

When it comes to crypto trading, it’s essential to understand capital gains and losses. Cryptocurrency is considered property by the IRS, making every buy, sell, or exchange a taxable event. This can result in either a capital gain or loss.

Reporting and Paying Taxes on Crypto Earnings

Do you pay taxes on crypto if you don’t sell? For U.S. taxpayers, simply holding onto crypto doesn’t incur taxes. Taxes are only reported and paid on earned or sold crypto. When selling, the profit from the sale is subject to tax based on your individual tax bracket.

Tax Exemptions

When you buy, sell or exchange crypto, it’s a taxable event. You report and pay taxes only on earned crypto or on sold/exchanged crypto. Tax is based on profit made from sale (sale price minus purchase price).

Tax Reporting

Understanding tax reporting for crypto trading is crucial. The IRS considers cryptocurrency as property, making every buy, sell, or exchange a taxable event, resulting in capital gains or losses. It is essential to accurately report and pay taxes on crypto earnings or transactions to comply with regulations.

| Tax Reporting |

| Calculating Tax on Crypto Profits The IRS treats cryptocurrency as property, so when you buy, sell, or exchange it, it counts as a taxable event. This often results in either a capital gain or loss. When it comes to holding crypto, there is no tax for simply holding it. However, you will only report and pay taxes on crypto that you’ve earned or purchased and later sold or exchanged for other crypto. If you incurred a loss from your crypto trading, you may still have to report it on your taxes. The amount of tax you have to pay on crypto profits depends on the profit you made from your sale, which is calculated by subtracting the original purchase price from the total sale price of your cryptocurrency. You’ll need to pay tax on this profit based on your personal tax bracket. |

| IRS Guidelines on Crypto Reporting The IRS classifies cryptocurrency as property, making cryptocurrency transactions taxable by law. You trigger capital gains or losses when you sell or use your crypto in a transaction if its market value has changed since you purchased it. Gains on crypto trading are treated like regular capital gains. Therefore, if you realize a gain on a profitable trade or purchase, you are required to pay taxes on it. It’s important to keep track of your crypto trading activities and report them accurately on your taxes to comply with IRS guidelines. Failing to report or pay taxes on your crypto trading can lead to penalties and other legal consequences. |

Tax Strategies

Crypto trading and taxes can be complex, but it’s important to understand how they work. The IRS treats cryptocurrency as property, meaning buying, selling, or exchanging it counts as a taxable event. This can result in a capital gain or loss, requiring you to report and potentially pay taxes on your crypto transactions.

| While trading cryptocurrencies, it’s important to understand how taxes work and implement tax strategies to minimize tax liabilities. The IRS treats cryptocurrency as property, meaning that buying, selling, or exchanging crypto is a taxable event that can result in capital gains or losses. Holding onto crypto without selling it doesn’t attract taxes. You only report and pay taxes on the crypto you earn, purchase, sell, or exchange. If you’ve experienced losses in crypto trading, you may need to report them on your taxes. The amount of tax you pay on crypto profits depends on your personal tax bracket and the difference between the sale price and the original purchase price. Gains from crypto trading are treated like regular capital gains, and they are taxable by law. Understanding these tax rules and working with a tax professional can help you navigate the complexities of crypto trading. |

Legal Compliance

Taxes on crypto trading are treated as taxable events by the IRS, resulting in either a capital gain or loss. Holding crypto without selling does not incur taxes, but earnings and sales of crypto are subject to reporting and payment of taxes.

| Legal Compliance |

| Responsibilities for Reporting Crypto Transactions to the IRS |

| When you engage in crypto trading, IRS regards it as taxable; each transaction could lead to a capital gain or loss. U.S. taxpayers must report earnings from selling or exchanging crypto, holding alone doesn’t incur tax. Calculate taxes based on profit, and remember that even losing money has reporting obligations. |

Frequently Asked Questions For How Do Taxes Work With Crypto Trading

How Is Crypto Trading Taxed?

The IRS taxes crypto trading as property, treating transactions as taxable events that result in capital gains or losses.

Do You Pay Taxes On Crypto If You Don’t Sell?

If you don’t sell crypto, you don’t pay taxes. Tax applies when selling or exchanging crypto, resulting in a capital gain or loss.

Do I Have To Report Crypto On Taxes If I Lost Money?

Yes, you must report crypto losses on taxes for potential benefits or offsetting gains.

How Much Tax Do You Have To Pay With Crypto?

You’re required to pay taxes on the profit made from selling crypto based on your tax bracket.

Conclusion

Understanding tax implications is crucial for crypto traders to avoid IRS penalties. Each transaction could result in capital gains or losses, affecting overall tax obligations. Properly reporting gains and losses is essential to ensure compliance and avoid tax-related issues. Stay informed and consult with a tax professional for guidance.